Corporate Treasury Adoption of Digital Assets: Financing Strategies, Market Reactions, and Advisor Incentives

Abstract

Since MicroStrategy's pioneering move in 2020 to adopt Bitcoin as a corporate treasury asset, listed firms across various sectors have explored similar strategies. This paper examines the financing mechanisms companies employ to acquire digital assets, the equity market's reaction to such announcements, and the role of external advisors in shaping outcomes. Using a dataset of 51 announcements between August 11, 2020, and August 11, 2025, we evaluate day-one and post-announcement stock performance relative to the referenced digital assets. Results indicate that equities frequently underperform the underlying tokens, with outcomes strongly influenced by company size, liquidity, and advisory incentives.

1. Introduction

The integration of digital assets into corporate treasuries represents a novel development in both financial strategy and capital markets. MicroStrategy's adoption of Bitcoin in August 2020 established a precedent for public companies, catalyzing similar moves across industries. These strategies often require substantial capital, which firms raise through equity or debt issuance.

This paper evaluates the financial structures underlying these decisions, analyzes how equity markets respond to treasury adoption, and explores the incentive structures of external advisors. Our dataset captures 51 public announcements spanning multiple digital assets, offering insight into the relationship between corporate equities and the volatile digital assets market.

2. Financing Mechanisms for Digital Asset Treasury

Equity Offerings

- At-the-Market (ATM) Offerings: Incremental share issuance directly into public markets at prevailing prices.

- Private Investments in Public Equity (PIPEs): Shares sold directly to accredited investors, often at a discount.

- Follow-on Public Offerings: Traditional secondary offerings of a fixed number of shares.

Debt Issuances

- Convertible Notes: Debt instruments convertible into equity, offering hybrid exposure. Widely used in Bitcoin treasury financing.

- Senior Secured Notes: Conventional debt backed by corporate assets, sometimes collateralized by the digital assets acquired.

3. Market Reactions: Aggregate Analysis

Overall Trends

- Announcement Day: Median stock return -3.67%; mean +10.9% (driven by a few outsized gains).

- Since Announcement: Median stock return -4.51% vs. +13.09% for tokens.

- Correlation: Equities and tokens exhibit high correlation (ρ ≈ 0.9), suggesting that many companies trade as levered digital asset proxies rather than on firm-specific fundamentals.

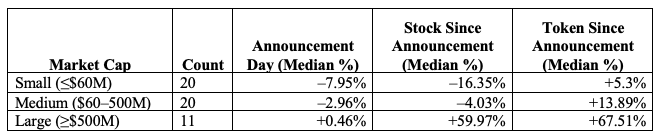

4. Market-Cap Effects

Market capitalization significantly shapes outcomes:

Interpretation: Larger firms benefit from liquidity and narrative durability, sustaining gains, while smaller firms suffer dilution and illiquidity.

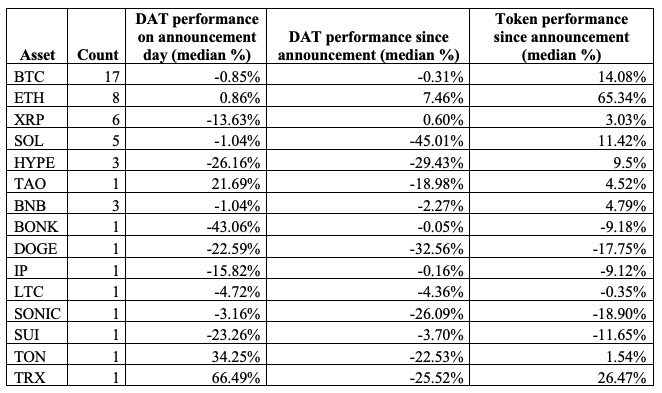

5. Asset-Specific Effects

Performance also depends on which digital asset is adopted:

- Bitcoin (17 cases): Median day-one -0.85%; stock since announcement -0.31% vs BTC +14.08%.

- Ethereum (8 cases): Day-one +0.86%; equities +7.46% vs ETH +65.34%.

- XRP (6 cases): Day-one -13.63%; equities +0.60% vs XRP +3.03%.

- SOL (5 cases): Day-one -1.04%; equities -45.01% vs SOL +11.42%.

- Smaller assets (HYPE, TAO, BONK, DOGE, etc.): Outcomes more volatile, with median equity underperformance relative to token.

Takeaway: Bitcoin dominates adoption, but Ethereum-linked announcements show stronger equity follow-through. Altcoin-linked treasuries are more speculative and less durable.

6. Discussion of Key Findings

- Large cap outperformance: Overall, large-market-cap association with tokens such as BTC and ETH tend to exhibit more sustainable returns and consistent performance compared to altcoins.

- No "Cheat Code" for Equity Performance: Median day-one returns are negative (-3.67%), and equities underperform their tokens post-announcement (-4.51% vs +13.09%).

- Equities as Leveraged Proxies: Investors treat many issuers as high-beta digital asset exposure, layering token volatility with additional equity risks such as dilution, governance, and operational execution.

- Importance of Scale: Larger firms can absorb volatility and maintain liquidity, while smaller firms are disproportionately punished by financing costs and narrative exhaustion.

- Confounding Factors: Announcement-day moves may reflect concurrent events (earnings, uplistings, financings), and illiquidity skews outcomes for microcaps.

7. Advisor Incentives and Conflicts

External advisors and sponsors play a pivotal role in structuring financing strategies such as PIPEs and ATM offerings. Their compensation typically includes:

- Upfront Fees: 1%-8% of the deal size.

- Long-Term Incentives: Multi-year stock options or warrants, often at negligible exercise prices.

While this model nominally ties advisor rewards to equity performance, it frequently benchmarks outcomes against the market-cap-to-net-asset-value (mNAV) ratio, defined as equity market capitalization relative to token treasury (NAV). The appeal of mNAV is its simplicity: it frames equity value as a premium over token holdings. However, its design creates a structural misalignment of interests:

- Denominator Risk: Because the denominator (NAV) can shrink when token prices fall, mNAV may appear to "improve" even if equity value has merely been sustained. For instance, if a company's token holdings decline in value but its market capitalization remains unchanged, the mNAV ratio rises. This merely reflects volatility in the denominator and shows little causality of genuine value creation.

This creates an incentive for advisors to focus on sustaining narrative-driven equity premiums rather than ensuring genuine, long-term value creation in treasury strategy. The compensation model therefore rewards optics over fundamentals. This dynamic helps explain why, across the sample, corporate equities have systematically failed to track the appreciation of their underlying tokens despite initial market enthusiasm.

8. Conclusion

The adoption of digital assets in corporate treasuries illustrates both the opportunities and potential pitfalls of financial innovation. The evolution of DATs reshape capital allocation across markets, attracting new investors to gain meaningful exposure in equity with digital asset underlying strategies. While firms continue to innovate and developed sophisticated financing mechanisms, equity markets remain skeptical, with most issuers underperforming the assets they purchase. Larger firms fare better, while smaller issuers face structural disadvantages.

A critical part of this dynamic lies in the evolution of the market-cap-to-net-asset-value (mNAV) framework, which first emerged with MicroStrategy's adoption of Bitcoin. In that case, Bitcoin was treated as a form of "stored value" or "reserve currency," allowing NAV to compound naturally with broader market adoption. However, when other tokens are adopted under the same lens, their suitability must be tested against first principles: does the asset function as a true store of value, or does its structure instead require sustainable yield generation to support NAV growth over time?

Future research should examine regulatory responses, long-term firm value effects, and the evolution of advisor incentives as digital asset markets mature.

Disclaimer: This document has been prepared for informational and research purposes only and does not

constitute, and should not be

construed as, investment advice, financial advice, trading advice, legal advice, or any other form of

professional advice. The

information contained herein is based on publicly available data, sources believed to be reliable, and the

author’s own

analysis, but no representation or warranty, express or implied, is made as to its accuracy, completeness,

or timeliness.

This document does not constitute an offer to sell, or a solicitation of an offer to buy, any securities,

digital assets, or other

financial instruments. It is not intended for distribution to, or use by, any person or entity in any

jurisdiction or country

where such distribution or use would be contrary to law or regulation.

Any views or opinions expressed are subject to change without notice and may not reflect the most current

developments.

They do not necessarily represent the views of Herring Global. Readers should not rely solely on the

information provided in

this document for any financial decision. You are solely responsible for conducting your own independent

research and due

diligence before making any investment or business decision.

Neither the author, nor Herring Global, nor any affiliated entity, shall be held liable for any losses,

damages, or claims arising

from the use of or reliance on this document.